WHY DO ESTATE PLANING?

1. Family succession and protection

You can plan during your life for succession by your family to you assets. You can arrange this as you wish and you can go on benefitting as

much and as long as you wish.

2. Ongoing control

You may wish to ensure that, whatever plans you make, you will keep control as long as you wish over your assets, including your companies

and businesses, and that those whom you wish will do so after you.

Special forms of Trust (sometimes combined with a Limited Partnership) and Foundations are the solutions used for this.

3. Asset Protection

By transferring your assets to a Trust or Foundation in an appropriate jurisdiction with appropriate law, there will be protection from claims by

your creditors (if any), if their causes of action arise after a stated period of time following the creation by you of the Trust or Foundation and

the transfer of property to it. Trusts and Foundations may also be used to prevent claims following divorce and to prevent foreign laws of

succession to your assets applying.

Trusts and Foundations are used for this purpose.

4. Avoidance of Probate

Probate is the piece of paper issued by the Court to give the executors of your Will authority to act.

The general rule is that the law of your domicile (the country or state in which you intend to live permanently) govern your Will.

However, if you have real property in other jurisdictions, it is the laws of those jurisdictions which governs the transfers of such real estate.

If you have assets situated in many jurisdictions, you may need to obtain in those jurisdictions either official approval of the Probate from the

jurisdiction of your domicile or new Probates issued in those jurisdictions. This process can be costly and time consuming.

If, during your life, you can create a Trust or Foundation, often combined with a company, to act as the “umbrella” for these assets, these

problems can be overcome.

In this respect it is necessary to look carefully first at any taxation implications regarding the transfer of the assets and the cost of doing so.

5. Legal mitigation of taxation

6. The need for a “back door”

Please remember that all good estate planning will seek to provide flexibility to meet changes of law or circumstance and changes in your

wishes and needs as well as the ability to undo or change the solutions you have adopted.

NOTE: This Memorandum is provided for your assistance but you should always take professional advice before acting. Circumstances and needs differ considerably from one person or family to another.

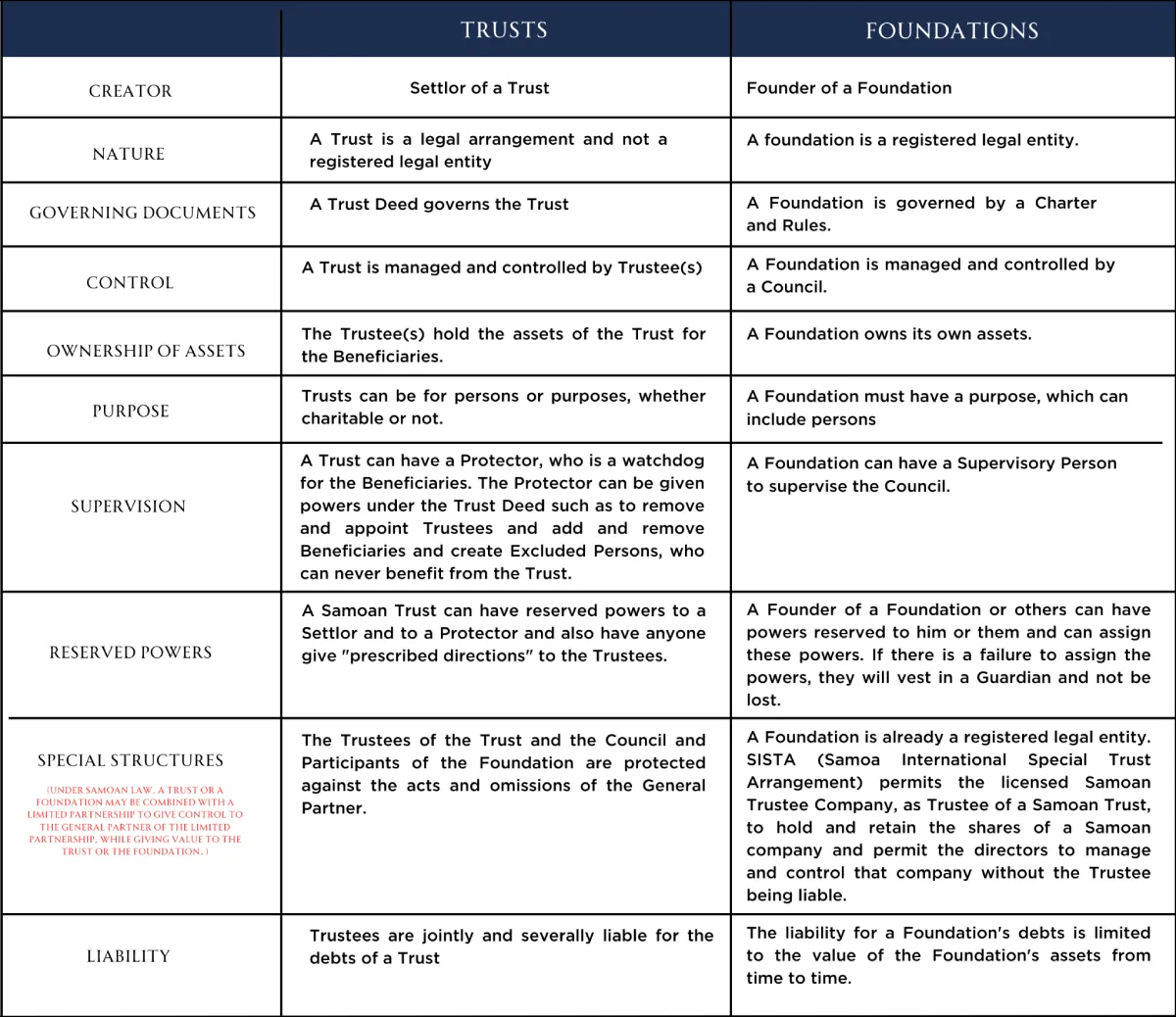

Comparison between Trusts and Foundations

Wills and Avoidance of Probate

1. The Value of Making a Will

2. Consequences of Not Making a Will

If you do not make a Will, then the rules of intestacy of the country will apply to determine who will receive what proportion of your estate and who will administer. Seldom do such rules provide that surviving spouse will receive everything and they may not otherwise provide what you wish regarding either who benefits or who will administer your estate.

3. Multi-Jurisdiction Wills

4. Understanding Probate

5. Special Cases and Considerations

The exception to the rule that the domicile of the client at the date of his death governs his Will is where he holds immovable property the transfer of which is governed by the law of the jurisdiction in which it is situated.

Therefore, it may be wise and practical to have Wills limited to the disposal of assets in each jurisdiction in which such immovable property is situated.

Other Wills limited to the disposal of assets in other jurisdictions can also be made by the client to cover the disposal of valuable assets without having to wait for the Probate of his main Will in the country of his domicile. This may save time and cost.

If the client has a main Will and limited Wills, disposing only of his property of whatever nature situated in stated jurisdictions, his main Will will dispose of all his property of whatever nature and wherever situated, except for the property of whatever nature situated in the jurisdictions of the limited Wills.

6. Trusts and Foundations

To avoid the need for Probate altogether, the client can transfer assets in his lifetime to the Trustees of a Trust or to a Foundation so that,

when he passes away, the assets transferred are no longer part of his estate, requiring a Will or Wills and Probate, but rather are trust assets or

assets of a Foundation already catering for succession to those assets.

Whether or not the creation of a lifetime Trust or a Foundation is appropriate will depend upon the cost of transfer of the assets concerned

and the taxation implications of such transfers and later when the assets are in the Trust or Foundation and when any Beneficiary receives a

distribution or benefit.