WORD FROM THE CEO

Talofa Lava and Greetings to you all in the mighty name of our Saviour Jesus Christ.

Welcome to the second edition of our INVEST SAMOA Newsletter. A lot has happened since the launch of our Newsletter in February 2018.

Our Asian Promotional INVEST SAMOA Seminar Series took us to Hong Kong and Singapore. Our Consultant Mr Thomas Mark Lea continued with our follow-up meetings in Dubai and Singapore.

INVEST SAMOA also successfully hosted a one (1) day Conference in Hangzhou Zhejiang University – China.

Some of the notable milestones in this part of the year’s work includes the revision of the INVEST SAMOA promotional events for the 2018/19 financial year.

While we explore avenues to promote we also continue to ensure we keep up with trends in the international market and most importantly comply with international standards.

This edition of our Newsletter brings you an update of activities implemented in Samoa since February 2018, upcoming events, legislative amendments completed, and proposed review of our international finance laws

to keep up with modern user

trends.

Meeting with the Samoa Law Society August 2018

S E N S I B L E

A P P R O P R I A T E

M O D E R N

O P T I M U M

A C C E S S I B L E

| SAMOA INTERNATIONAL |

| Foundations International Banks International Business Companies International Insurance International Partnerships & Limited Partnership International Mutual Funds Segregated Fund International Companies Special Purpose International Companies Trusts |

SRS REGISTRATION — DUAL LANGUAGE UP DATE

Why Samoa?

In keeping up with the development of technology, as well as the constant change, the Samoa International Finance Authority (SIFA) conducted an update of its systems to allow efficiency and speed of delivery for SIFA staff as well as ease of doing business for Trustee companies .

An additional function has been added to the SIFA Registration System (SRS). Trustee Companies can now submit via the SRS system a request for the issue of a dual language certificate.

The function replaces Trustee Companies having to physically file the request and certificate of translation, and registry staff no longer have to manually apply the translations onto the certificates before printing. This will significantly save time and costs on both sides.

SIFA strives for efficient response times for its customers without comprising security of information. The new addition to the SRS is a step towards developing electronic systems, and making systems more user-friendly

Meeting with Trustee Company Service Providers – February 2018

COMMON REPORTING STANDARDS IMPLEMENTATION — SAMOA

COMMENTARY

Samoa formalized its commitment to the CRS of the OECD for all Samoan international financial entities namely international companies, trusts, foundations,

international partnerships and limited partnerships or legal arrangements offered by SIFA and provided by local trustee companies (TCSP’s) in July 2018.

In the wake of the implementation of the CRS

standard, this article provides an update as to the status of CRS and how it has come about in Samoa.

The rationale behind the CRS initiative dates to collective action by the G20, G8 and OECD whereby they developed a global standard for jurisdictions to move towards automatic exchange of information and to improve the availability, the quality and the accuracy of information on beneficial ownership, in order

to effectively act against tax fraud and evasion on 22 May 2013. It is safe to say that

the focus of the CRS is on financial accounts information of all financial entities to be reported to the tax authorities.

According to the OECD, a jurisdiction implementing the CRS must have rules in place

that require financial institutions to report information consistent with the scope of reporting set out in Section I and to follow due

diligence procedures consistent with the procedures contained in Section II through to VII1. For Samoa, the legislative framework is now in place with the passage of recent amendments to the Tax Information Exchange Agreement Act 2017 incorporating the international standard on exchange of information.

For CRS in Samoa, we focus on the type of information that is required to be exchanged which continues to be the center of debate due to different interpretations/ commentaries on the type of information that is to be reported. One certainty is that trustee companies are captured by CRS due to the nature of their business activity which is covered by the definition of Custodial institutions and investment entities. It appears however that the rest of CRS implementation may remain obscure for several reasons. For entities governed by SIFA, they have been categorized as financial institutions (FIs) as follows:

Custodial institutions

Depository institutions

Investment entities

Specified insurance companies

The OECD however has stated that FIs will not be captured by CRS if they can show a low risk of being used for evading tax and are excluded from reporting. How FI’s can show low risk is another obscurity for us to uncover.

Financial information to be reported with respect to reportable accounts includes:

Interests

Dividends

Account balance

Income from certain insurance products

Sales proceeds from financial assets

Other income generated with respect to assets held in the accounts or payments made with respect to the account

Reportable accounts are accounts held by individuals and entities (trusts and foundations, companies, partnerships). Applying this definition means that certain international entities may not be required to report for CRS due to the absence of accounts being held here in Samoa. Furthermore, CRS also proposes to look through passive entities to report on the relevant controlling persons. 2Passive entities includes a partnership or trust other than a business trust for the whole accounting period on which the tax is based. Controlling persons is defined in Section VIII (D) (6) of the CRS as meaning the natural persons who exercise control over the entity with some elaboration on how this would apply to trusts. Additionally, controlling persons under CRS is also interpreted in line with the Financial Action Task Force Recommendations which are incorporated into Samoa’s Anti Money Laundering legal framework. For custodial accounts, CRS is after information such as the total gross amount of interest, total gross amount of dividends and total gross amount of other income generated with respect to the assets held in the account during the calendar year or other appropriate reporting period. It is safe to say that none of these are found in Samoa.

Given companies are Samoa’s most popular solution, CRS requirements for companies has caused another ambiguousness. For example, Company information to be reported are information such as the name, address, jurisdiction of residence, TIN number, date and place of birth for reportable individuals or account holders that set up a company. An important point to note is that companies meet the definition of Financial Institution if it holds itself out as an investment fund or similar investment vehicles if investors participate either through debt or equity in investment schemes through the holding company. However, it is also noted that there are quite a lot of determinations to be made before a company is deemed to be a reporting entity for CRS purposes as each type of entity has different components to determine whether a company is a reporting entity as well as the type of information that it must report.

Like companies, similar information is required of Trusts set up by local professionals as well as partnerships. Each jurisdiction may allow for a Reporting FI to use service providers to fulfil the reporting and the due diligence obligations imposed on such Reporting FIs, as contemplated in domestic law, but these obligations shall remain the responsibility of the Reporting FI3. In the same regard, there is a long determination process regarding the type of information and whether such entity i.e. Trust or Partnership must report for CRS purposes.

Conclusion

The due date for CRS reporting here in Samoa was 21st September 2018. We now await how the OECD will assess Samoa’s implementation of CRS given this is the first round as we have identified some interesting points of development in the progress of the reports completed. Despite the uncertainty and various commentaries on CRS obligations, we are certain that there will be an influx of requests for information and such requests will continue to alter the way the OECD implements its initiative for jurisdictions to further open up. At the same time, Samoa will continue to explore ways to ensure compliance will work for the mutual benefit of the users of the jurisdiction, as well as the international standard setters.

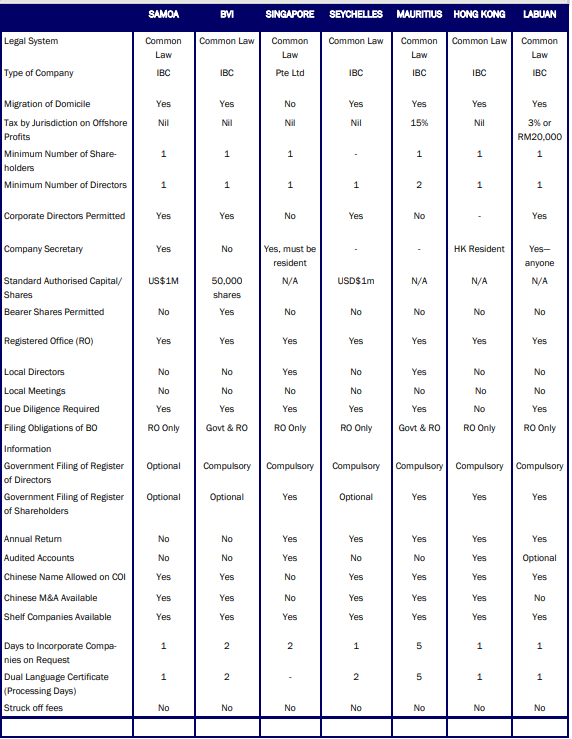

SAMOA INTERNATIONAL BUSINESS COMPANIES COMPARISON

SAMOA AND THE EU LISTING

The year 2017 saw the European Union (EU) release a list of non-EU members that it found to be noncooperative jurisdictions on tax matters.

Samoa was one of the seventeen (17) countries on the EU’s December 2017 list. Despite Samoa being successfully reviewed by the OECD’s Global Forum on Tax and the Financial Action Task Force (FATF) Asia Pacific Group (APG) for AML/CFT in 2017 and 2015 respectively.

Samoa and all other listed offshore jurisdictions have contested the list. Samoa is in dialogue with representatives of the EU commission, while continuing its preparations towards its review by the Organisation for Economic Co-operation and Development (OECD), to be launched in the third quarter of 2018, under the OECD’s 2016 Terms of Reference.

A mock onsite was conducted in May 2018 in preparations for the OECD review. As a result, a review of the Trustee Companies Regulations 2018 was conducted to address the issue of updating information on beneficial owner’s records.

Samoa prides itself in its leading efforts to maintain regulated and supervised international financial solutions. It will continue to maintain its efforts in order to comply with international standards, and maintain its credibility as a competent jurisdiction of choice for offshore services.

The Registrar of International Companies (Samoa International Finance Authority) has conducted various compliance activities.

Moreover, Samoa as a jurisdiction offering international financial services has allocated time, resources and efforts in order to ensure Samoa’s offshore business is appropriately regulated and supervised.

This is made evident through its legislative amendments to meet the international standards set by various international bodies Samoa is a member of including: the OECD, FATF/ Asia Pacific Group on Money Laundering (APG), Group of International Finance Centre Supervisors (GIFCS) and the International Association of Insurance Supervisors (IAIS).

INVEST SAMOA

CALENDAR OF EVENTS

| 11th November 2018 Society of Trusts and Estate Practitioners (STEP), Arabia , Abu Dhabi 13th—15th November 2018 China Offshore Summit, Shanghai 20th – 21st November 2018 Society of Trusts and Estate Practitioners (STEP), Hong Kong 28th—30th April 2019 Offshore Alert Conference |

LEGISLATIVE REVIEWS

To consolidate Samoa’s compliance with international standards the Trustee Companies Regulations 2018 (“the Regulations”) has been introduced to address the issue of maintaining and updating beneficial owner’s records for all entities or vehicles that a Trustee company administers.

The amendment also brings Samoa into conformity with regulation 5 of the Money Laundering Prevention Regulations 2009.

Another important aspect of the Regulations is further strengthening Samoa’s compliance regime to ensure that accounting records of vehicles are kept.

Upcoming Reviews:

Proposed review to the Trustee Companies Act 2017 to ensure Samoa adheres to the highest standards of the OECD and Asia Pacific Group (APG) on Anti-Money Laundering (AML). There are also plans to re

Above: Discussion Panel consisting of Professors and Experts in Wealth Management—INVEST SAMOA Hangzhou Seminar

Right: Invest Samoa Seminar Presentation—

Hong Kong Foreign Correspondents’ Club (FCC)

CONTACT US

Level 6

Development Bank of Samoa Building

Apia

SAMOA

Phone: +68566400/ +68566412

Fax: +68520880

Email: info@investsamoa.ws

Facebook: facebook.com/investsamo

Above: CP Global Group Visit—September 2018